Adobe wanted to write a massive check. Synthesia wanted more. Now both companies face an awkward question: what happens next?

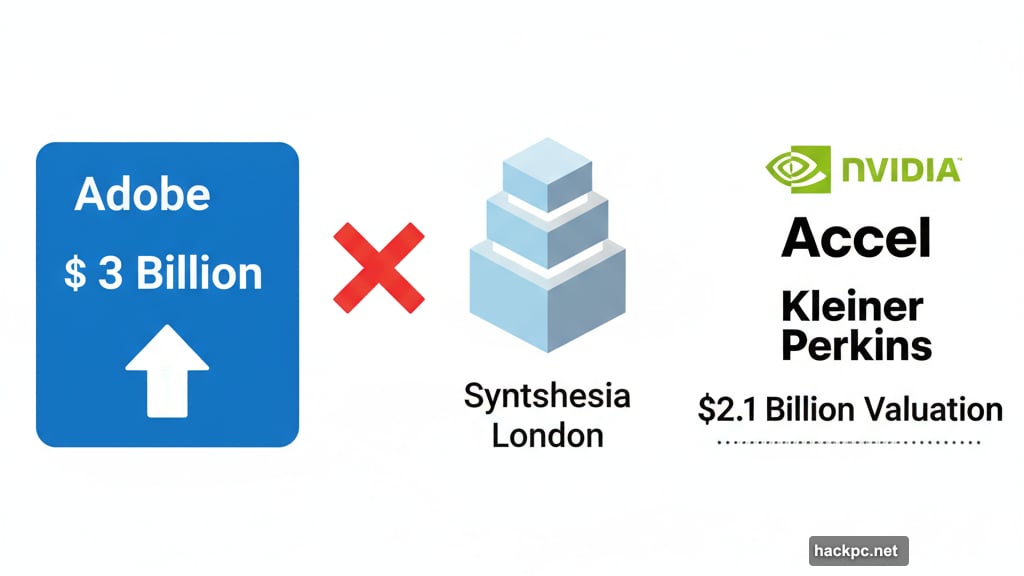

The creative software titan reportedly pursued London-based Synthesia in recent months, offering around $3 billion to acquire the AI video startup known for its avatar technology. But the deal collapsed over price disagreements, according to The Information.

This wasn’t just another failed acquisition. It reveals Adobe’s urgent push to dominate AI-generated video before competitors leave them behind.

The Deal That Almost Was

Adobe’s interest in Synthesia makes perfect sense. The startup lets anyone create professional videos by typing a script, choosing an avatar, and selecting a voice. No cameras. No actors. No production crew.

Behind that simplicity sits sophisticated tech that generates realistic, lip-synced avatars speaking 120+ languages. Plus, Fortune 100 companies love it—over 70% use Synthesia for training videos, corporate announcements, and marketing content.

So Adobe saw an opportunity to instantly own a proven enterprise platform. Instead of building avatar technology from scratch, they could acquire a company already generating $100 million in annual recurring revenue.

But Synthesia’s investors valued the company at $2.1 billion after a Series D round in January 2025. Adobe’s $3 billion offer represented a 43% premium. Yet both sides still couldn’t agree on terms.

Adobe’s AI Video Problem

Here’s the uncomfortable truth: Adobe is playing catch-up in AI video.

Runway secured investments from Google and Salesforce Ventures. OpenAI’s Sora set new standards for text-to-video realism. Meanwhile, Adobe relies primarily on Firefly and incremental AI features added to Photoshop and Premiere Pro.

Those tools are impressive. But they don’t compete directly with avatar-based video creation, which is exploding in corporate communications and training sectors.

Moreover, startups move faster than legacy software giants. Synthesia doubled its revenue year-over-year while Adobe navigated internal bureaucracy and integration challenges.

Buying Synthesia would have solved both problems—instant market leadership and proven technology. Instead, Adobe faces the same dilemma it had before the talks began.

Synthesia’s Strategic Position

Founded in 2017, Synthesia grew from academic research into a commercial powerhouse. The company raised over $330 million from heavyweights like Nvidia, Accel, and Kleiner Perkins.

Its growth trajectory is remarkable. Revenue hit $100 million in annual recurring revenue by April 2025, doubling from the previous year. That kind of momentum attracts serious attention.

Yet the company remains unprofitable. Financial filings showed a £25.2 million pre-tax loss on £25.7 million revenue for 2023. CEO Victor Riparbelli acknowledged this but emphasized the company has “a clear path to profitability backed by solid cash reserves.”

Still, rejecting a $3 billion offer while operating at a loss is bold. It signals confidence that valuation will climb higher—or reveals concerns about losing control to a major acquirer.

The Figma Shadow

This isn’t Adobe’s first failed mega-deal. Last year, regulators blocked its $20 billion acquisition of Figma, the design platform that threatened Adobe’s dominance in creative tools.

That collapse stung. Adobe lost a chance to eliminate a rising competitor and faced criticism for attempting anti-competitive consolidation.

Now the Synthesia situation raises similar questions. Can Adobe grow through acquisition without triggering antitrust scrutiny? Or must it rely entirely on internal innovation?

The company already invested in Synthesia through its venture arm earlier this year, calling it a “strategic partnership to democratize high-quality content creation.” That investment suggested acquisition interest even then.

So Adobe faces a tricky balance: pursue aggressive M&A while regulators watch closely, or build everything internally and risk falling behind nimbler competitors.

What Happens Next

The failed talks don’t necessarily end Adobe’s relationship with Synthesia. The existing investment and partnership could expand into deeper collaboration without a full acquisition.

For Synthesia, the validation matters. Adobe’s $3 billion offer confirms its technology and market position. That strengthens its hand in future fundraising or acquisition discussions.

Meanwhile, Adobe must decide its next move. Keep building Firefly and native AI tools? Pursue other AI video startups? Or circle back to Synthesia with a higher bid?

The pressure is real. Generative AI is reshaping content creation faster than anyone predicted. Professional video that once required days and thousands of dollars now takes minutes and costs pennies.

Companies that master this transition will dominate creative software for the next decade. Those that hesitate risk obsolescence.

Adobe knows this. Synthesia knows this. So the question isn’t whether they’ll work together somehow—it’s on whose terms and for how much.

The $3 billion offer may have failed. But the underlying tension remains: Adobe needs what Synthesia built, and Synthesia wants to stay independent while it can.

That tension won’t resolve quickly. And in the meantime, competitors aren’t waiting.

Comments (0)