Adobe just wrapped up its annual conference in Los Angeles. Thousands of marketers, filmmakers, and content creators showed up. But the real story isn’t what happened on stage.

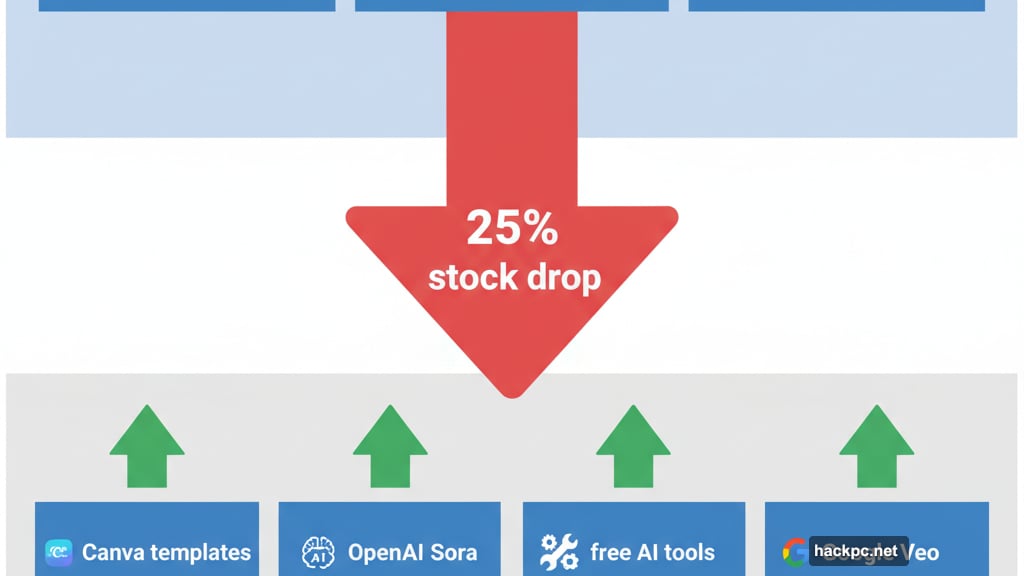

Wall Street isn’t buying Adobe’s AI pitch. The stock dropped 25% this year while competitors surge ahead. Investors worry that the same AI tools Adobe embraced might actually destroy its business model.

Here’s the uncomfortable truth Adobe faces right now.

The Problem Everyone Sees Coming

Citi analyst Tyler Radke didn’t mince words. Adobe faces “structural competition and pricing pressure driven by AI.” That’s analyst-speak for “your business might be fundamentally broken.”

The creative software market is transforming faster than Adobe can adapt. People who once needed Photoshop now use free AI tools instead. Social media videos? Created with OpenAI’s Sora. Party invitations? Designed on Canva templates. Professional software isn’t required anymore.

Plus, this shift accelerates daily. Ordinary people create professional-looking content without touching Adobe products. That’s terrifying for a company built on selling expensive creative software subscriptions.

Adobe’s Stock Tanks While AI Booms

Adobe isn’t alone in struggling. Salesforce and Workday face similar investor skepticism. But Adobe’s situation carries unique risks.

Most enterprise software companies worry that customers adopt AI slowly. Adobe faces the opposite problem. AI adoption in creative work happens rapidly—just not with Adobe’s tools.

CEO Shantanu Narayen claims the market unfairly punishes Adobe. He argues investors obsess over semiconductors and AI training while undervaluing application software. But the numbers tell a different story. When competitors gain ground this quickly, something’s genuinely wrong.

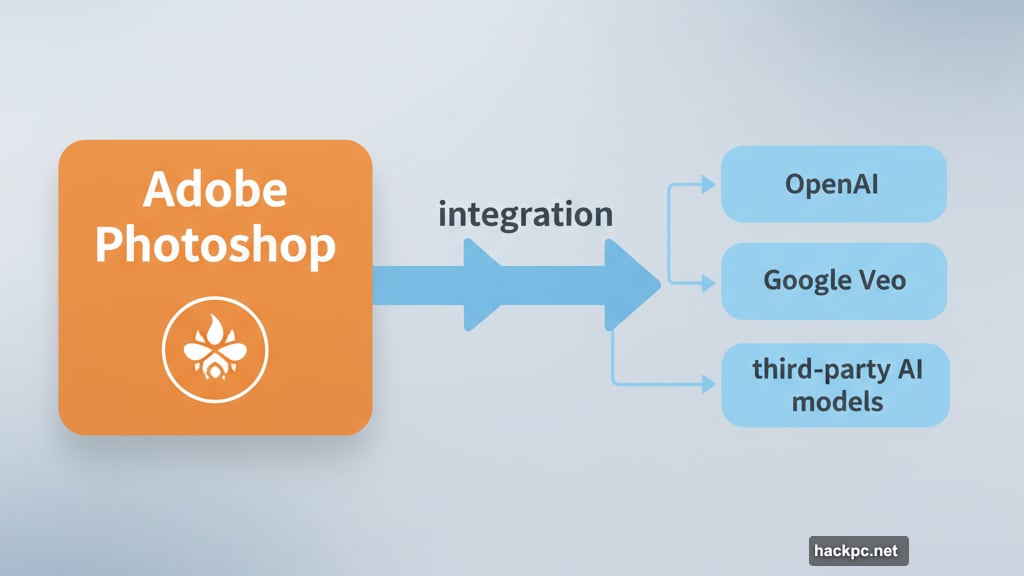

Meanwhile, Google’s Veo video model and other AI tools reshape creative workflows. Adobe built an empire on professional tools that took years to master. Now anyone can produce similar results in minutes using competitor products.

The Strategic Pivot Nobody Expected

Adobe made a surprising move at this week’s conference. The company integrated competitor AI models—including Google and OpenAI—directly into Photoshop and other core products.

Think about that shift. Adobe spent years promoting its Firefly AI model. The company emphasized copyright safety and appropriate content. Now it’s essentially becoming an AI model distributor, bulk purchasing third-party services for customers.

Ely Greenfield, Adobe’s Creative Business CTO, explained the reasoning. “People have gradually come to accept the reality that models require training on vast amounts of data.” Translation: customers don’t care about Adobe’s safety pitch anymore. They want the best tools regardless of source.

So Adobe changed strategies. Clients now use Firefly for formal published content. But they experiment with third-party models during creative ideation. Adobe supplies both options rather than fighting this reality.

The Revenue Numbers Don’t Add Up

Adobe claims AI-focused products generate over $250 million annually. Sounds impressive until you realize that’s a tiny fraction of the company’s $19 billion yearly revenue.

The company introduced a broader metric called “AI-driven revenue.” This estimates AI technologies contribute roughly $5 billion annually by improving pricing or reducing customer churn. But that number feels suspiciously fuzzy.

KeyBanc analyst Jackson Ader noted conference attendees responded positively to third-party AI model integration. He remarked: “We endorse this strategy; previously, we questioned whether Adobe could maintain a competitive edge in AI-driven image and video generation.”

That statement reveals the core problem. Analysts doubted Adobe’s AI competitiveness. The new strategy addresses concerns but doesn’t solve them. Adobe went from creating AI tools to distributing everyone else’s AI tools. That’s not a position of strength.

What This Means for Creative Professionals

Conference attendees seemed enthusiastic about accessing multiple AI models through Adobe products. That makes sense from a user perspective. Why juggle different platforms when Adobe provides everything in one place?

But this convenience carries hidden costs. Adobe essentially admits its own AI can’t compete with OpenAI and Google. So professionals now depend on Adobe’s relationships with those companies. If those partnerships sour, workflows break.

Moreover, pricing remains unclear. Adobe purchases AI services in bulk then resells to customers. How much markup exists? Nobody knows yet. History suggests Adobe won’t undercut its profit margins to help users save money.

The broader concern involves creative work commoditization. When AI makes professional content creation accessible to everyone, what happens to professionals? Adobe hasn’t answered that question satisfactorily.

The Skepticism Makes Sense

Evercore ISI analyst Kirk Materne called this year’s conference “another critical step in addressing market concerns about whether generative AI poses an existential threat” to Adobe. Notice he didn’t say Adobe solved those concerns. Just addressed them.

That distinction matters. Adobe demonstrated awareness of the problem. The company adjusted strategy accordingly. But fundamental questions remain unanswered.

Can Adobe maintain premium pricing when free alternatives proliferate? Will professional creators continue paying subscriptions? Does distributing competitor AI models create sustainable competitive advantage? Nobody knows yet.

So investors stay skeptical. Adobe’s stock reflects that uncertainty. The company might adapt successfully. Or AI might fundamentally disrupt creative software the same way smartphones destroyed point-and-shoot cameras.

Adobe Faces an Uncomfortable Truth

The creative software market Adobe dominated for decades is vanishing. Not slowly—rapidly. AI tools democratize content creation in ways Adobe can’t reverse or control.

Adobe’s response involves embracing competitor AI rather than fighting it. That’s pragmatic but problematic. The company went from technology leader to technology distributor. That’s a massive strategic retreat disguised as partnership.

Customers might appreciate convenience. But investors see vulnerability. When your main value proposition becomes packaging other companies’ innovations, you’re not indispensable anymore.

Adobe still has advantages. Massive user base. Industry relationships. Integration capabilities. Professional workflows built around its products. Those moats offer protection. But AI erodes them faster than anyone expected just two years ago.

The survival question isn’t whether Adobe continues existing. The company has resources to adapt. The real question involves relevance. Will Adobe remain central to creative work, or become just another distribution channel for AI tools actually driving innovation?

Right now, investors bet on the latter. Adobe needs to prove them wrong before skepticism becomes reality.

Comments (0)