Managing personal finances has evolved from spreadsheet juggling to sophisticated digital ecosystems that transform how we interact with money. After extensive testing of both Quicken Simplifi and YNAB (You Need A Budget), I’m ready to dissect these financial powerhouses and help you determine which budgeting solution deserves your monthly subscription dollars.

The Financial Technology Revolution Nobody Saw Coming

Remember when budgeting meant scribbling numbers on the back of envelopes? Those days feel like ancient history now. Modern money management software has become the financial equivalent of having a personal CFO in your pocket, automatically categorizing transactions, projecting cash flow scenarios, and sending real-time alerts about spending patterns.

The competition between Quicken Simplifi and YNAB represents more than just feature lists—it’s a philosophical battle between automated simplicity and hands-on financial education. Each platform attracts devoted users who swear by their chosen methodology, creating passionate communities that rival sports fandoms in their intensity.

Breaking Down the Contenders: Background & Philosophy

Quicken Simplifi: The Modern Minimalist’s Dream

Launched in 2020 by Quicken Inc., Simplifi emerged as the company’s answer to millennials and Gen Z users who found traditional Quicken Classic overwhelming. This cloud-based personal finance app strips away complexity while maintaining powerful functionality, offering automated spending plans that adapt in real-time to your financial behavior.

The platform’s core philosophy revolves around effortless money management. Rather than forcing users into rigid budgeting frameworks, Simplifi creates personalized spending plans based on your income, bills, subscriptions, and savings goals. It’s financial management for people who want results without micromanagement.

YNAB: The Zero-Based Budgeting Evangelist

Since 2004, YNAB has cultivated an almost cult-like following through its distinctive approach to personal finance management. The platform doesn’t just track money—it fundamentally changes how users think about every dollar they earn. Built on four core rules (Give Every Dollar a Job, Embrace Your True Expenses, Roll With the Punches, and Age Your Money), YNAB transforms budgeting from passive tracking into active financial planning.

This zero-based budgeting system requires users to allocate every incoming dollar before spending occurs, creating intentional money management habits that often lead to dramatic financial transformations. Users frequently report saving $600 in their first two months and over $6,000 in their first year.

Pricing Structure: The Real Cost of Financial Clarity

Quicken Simplifi Pricing (2025)

- Annual Subscription: $47.88/year (frequently discounted to $35.88)

- Monthly Breakdown: $3.99/month when billed annually

- Trial Period: 30-day money-back guarantee

- Promotional Offers: New users often receive 40-50% off first year

YNAB Pricing (2025)

- Monthly Plan: $14.99/month

- Annual Plan: $109/year (saving $71 annually)

- Trial Period: 34-day free trial (no credit card required)

- Student Discount: Free for one year for verified college students

The price differential reflects fundamentally different value propositions. Simplifi positions itself as affordable financial tracking for the masses, while YNAB justifies its premium pricing through educational resources, live workshops, and a methodology that promises substantial savings returns.

Feature Comparison: Where the Rubber Meets the Road

Account Connectivity & Transaction Management

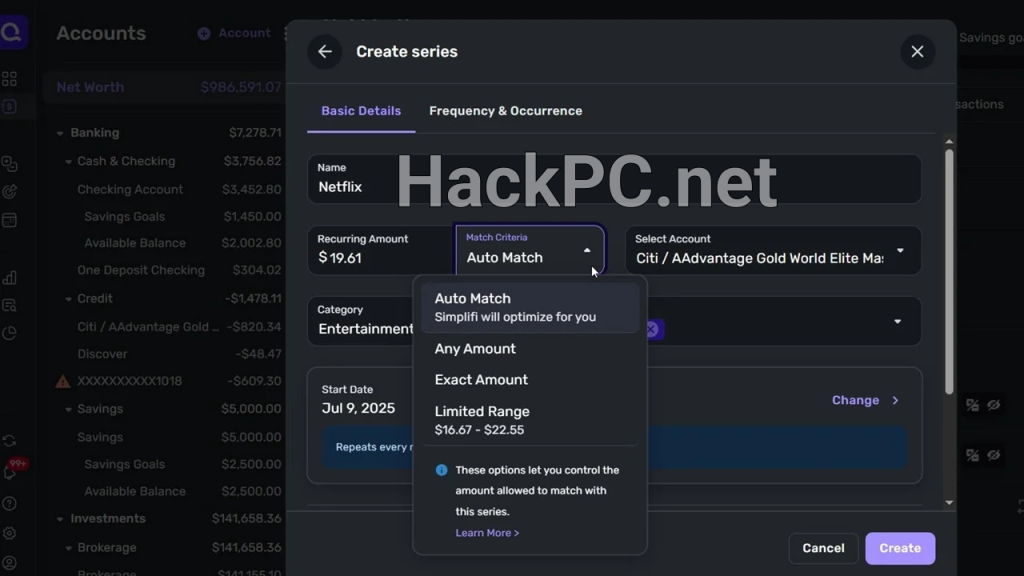

Quicken Simplifi excels in seamless bank account integration, supporting over 14,000 financial institutions through secure connections. The platform automatically downloads and categorizes transactions, with intelligent recognition that improves over time. Investment account tracking includes real-time quotes, performance analysis, and portfolio visualization that rivals dedicated investment platforms.

YNAB takes a more selective approach to connectivity, prioritizing reliability over quantity. While supporting fewer institutions than Simplifi, YNAB’s connections tend to be more stable. The platform encourages manual transaction entry for increased awareness, though automatic import remains available for those who prefer convenience.

Budgeting Methodology & Financial Planning

Simplifi’s Spending Plan represents a revolutionary departure from traditional budgeting. Instead of rigid categories, the system creates a dynamic framework that shows available spending money after accounting for bills, subscriptions, and planned savings. The projected cash flow feature provides 12-month forecasts, helping users anticipate financial bottlenecks before they occur.

YNAB’s Zero-Based Approach requires more initial setup but delivers profound behavioral changes. Every dollar receives an assignment—whether for immediate expenses, future obligations, or long-term goals. The “Age Your Money” metric gamifies financial stability, encouraging users to extend the time between earning and spending money.

Investment Tracking & Wealth Building

Quicken Simplifi shines in investment management, offering:

- Complete portfolio overview with asset allocation analysis

- Cost basis tracking for tax optimization

- Performance metrics comparing returns against benchmarks

- Dividend tracking and reinvestment monitoring

- Zillow integration for real estate valuation

YNAB deliberately minimizes investment features, focusing instead on cash flow management and debt elimination. While you can track investment account balances, detailed portfolio analysis requires third-party tools. This limitation reflects YNAB’s philosophy that budgeting basics should precede investment complexity.

Mobile Experience & Cross-Platform Functionality

Both platforms prioritize mobile-first design, recognizing that financial management happens everywhere. Simplifi’s iOS and Android apps mirror the web interface completely, with responsive design that adapts seamlessly across devices. The spending watchlist feature sends customized alerts about problematic spending patterns, helping users stay accountable throughout the day.

YNAB’s mobile applications receive consistent praise for intuitive navigation and quick transaction entry. The platform’s emphasis on frequent engagement translates into mobile features optimized for rapid budget consultations and on-the-go adjustments.

Advanced Features That Set Them Apart

Quicken Simplifi’s Standout Capabilities

Refund Tracking: Automatically monitors and alerts users when refunds post to accounts—a seemingly simple feature that saves countless hours of manual verification.

Subscription Management: Comprehensive tracking of recurring charges with cancellation reminders and spending analysis helps users identify forgotten subscriptions draining their accounts.

Tax Report Automation: New 2025 feature automatically generates categorized expense reports for tax preparation, integrating seamlessly with popular tax software.

Retirement Planner: Web-exclusive tool allows scenario modeling with multiple variables, helping users visualize different retirement pathways.

Bill Connect: Automatic synchronization with credit card companies ensures payment tracking accuracy without manual entry.

YNAB’s Unique Advantages

YNAB Together: Share subscriptions with up to six people at no additional cost, perfect for families or accountability partners managing collective finances.

Loan Planner: Sophisticated debt payoff calculator shows exactly how extra payments reduce interest and accelerate freedom from debt.

Educational Ecosystem: Free workshops, video courses, and active community forums provide ongoing financial education beyond software features.

Goal Tracking Flexibility: Multiple goal types (target balance, monthly contribution, target date) accommodate various saving strategies and timelines.

Credit Card Management: Revolutionary approach to credit card budgeting prevents debt accumulation by treating charges as cash transactions.

User Experience & Learning Curves

Simplifi: Instant Gratification Meets Long-Term Value

New users typically achieve full setup within 30 minutes, with meaningful insights appearing immediately after account connection. The platform’s automated categorization reduces ongoing maintenance to under five minutes weekly. The clean, colorful interface makes financial data approachable rather than intimidating.

Customer support responds within minutes through chat, with phone callbacks available for complex issues. The knowledge base covers common scenarios comprehensively, though advanced features sometimes lack detailed documentation.

YNAB: Investment in Education Pays Dividends

The initial learning curve spans several weeks as users internalize the methodology. YNAB’s approach requires philosophical shifts that challenge conventional financial thinking. However, this investment yields profound results—users report fundamental changes in their relationship with money.

Support extends beyond technical assistance to include budgeting coaching through workshops and forums. The Reddit YNAB community (205,000+ members) provides peer support that often surpasses official channels in helpfulness.

Security & Privacy Considerations

Both platforms implement bank-level security with 256-bit encryption and multi-factor authentication. Neither sells user data to third parties—a critical distinction from free alternatives that monetize through advertising and data brokerage.

Simplifi leverages Quicken’s 40-year security infrastructure, with SOC 2 Type II certification and regular third-party audits. Read-only bank connections prevent unauthorized transactions.

YNAB partners with Plaid, MX, and TrueLayer for secure banking connections, maintaining PCI DSS compliance for payment processing. The platform’s privacy-first approach includes options for completely manual operation without bank connections.

Real-World Performance: Success Stories & Limitations

Quicken Simplifi Success Patterns

Users consistently praise Simplifi for revealing spending patterns invisible in banking apps. The spending watchlist feature helps Amazon addicts and impulse buyers identify triggers and establish boundaries. Small business owners appreciate the ability to track business expenses alongside personal finances without complex segregation.

Investment-focused users find particular value in Simplifi’s portfolio tracking, with several reporting improved investment decisions based on performance insights. The net worth tracking feature, enhanced by real estate integration, provides motivating progress visualization.

YNAB Transformation Stories

YNAB’s impact stories border on miraculous—users regularly report eliminating decades of debt, funding dream vacations, and achieving financial independence years ahead of schedule. The methodology’s emphasis on true expenses prevents the feast-or-famine cycles that plague reactive budgeters.

College students using YNAB’s free program develop financial skills that prevent post-graduation debt accumulation. Couples report reduced financial friction through shared understanding and collaborative goal-setting.

The Verdict: Choosing Your Financial Companion

Choose Quicken Simplifi If You:

- Want automated budgeting with minimal manual input

- Manage investments alongside everyday finances

- Prefer visual dashboards over detailed reports

- Need quick setup without extensive learning

- Track business and personal finances together

- Value comprehensive features at budget pricing

Choose YNAB If You:

- Commit to transforming your financial habits

- Struggle with overspending or debt cycles

- Want detailed control over every dollar

- Value education and community support

- Need accountability through active engagement

- Believe premium pricing reflects premium value

Alternative Considerations

While Simplifi and YNAB dominate their respective niches, alternatives deserve mention. Monarch Money combines elements of both approaches with collaborative features. Mint‘s discontinuation pushed many users toward these paid alternatives, validating the subscription model’s sustainability.

Rocket Money (formerly Truebill) excels at subscription management and bill negotiation but lacks comprehensive budgeting depth. PocketGuard simplifies budgeting further than Simplifi but sacrifices customization flexibility.

Implementation Strategy: Maximizing Your Choice

Regardless of platform selection, success requires commitment beyond software features. Start with a clear financial inventory—list all accounts, debts, and recurring obligations. Set specific, measurable goals with realistic timelines.

For Simplifi users, begin with the spending plan and gradually explore investment tracking and reporting features. Let automation handle routine tasks while focusing attention on spending patterns and goal progress.

YNAB users should embrace the full methodology rather than cherry-picking features. Attend workshops, engage with the community, and trust the process even when it feels uncomfortable initially.

The Future of Personal Finance Management

Both platforms continue evolving with user needs. Simplifi’s 2025 roadmap includes AI-powered spending predictions and enhanced business features. YNAB explores collaborative budgeting expansions and international banking improvements.

The broader trend toward financial democratization suggests these tools represent early iterations of comprehensive financial operating systems. As open banking regulations expand globally, expect deeper integration with financial services beyond simple tracking.

Final Thoughts: Your Money, Your Choice

The Simplifi versus YNAB decision ultimately reflects personal philosophy about money management. Simplifi offers elegant simplicity for users wanting financial clarity without lifestyle disruption. YNAB provides transformational methodology for those ready to fundamentally restructure their financial habits.

Both platforms justify their subscription costs through tangible savings and reduced financial stress. The winner isn’t the platform with more features or lower pricing—it’s the one that successfully changes your financial trajectory.

Start with free trials for both platforms. Import your accounts, explore the interfaces, and pay attention to which approach resonates with your financial personality. The best budgeting app is the one you’ll actually use consistently.

Remember: these tools are investments in your financial future. Whether you choose Simplifi’s automated elegance or YNAB’s methodical transformation, you’re taking control of your money rather than letting it control you. That decision alone puts you ahead of the 60% of Americans living paycheck to paycheck.

Comments (0)